2026 Beginner's Guide: What Are On-Chain Assets? From Wallets to RWA, One Article to Understand Core Concepts

What are on-chain assets? How to choose a wallet? What is RWA? This 2026 beginner's guide explains core concepts in plain language, helping you start from zero without detours. Includes detailed FAQ and practical advice.

Table of Contents

- You May Have Already Encountered On-Chain Assets

- Part 1: What Exactly Are On-Chain Assets?

- Part 2: Wallets—Your Digital Asset Safe

- Part 3: RWA—Real World Assets on the Blockchain

- Part 4: How to Play with On-Chain Assets? Beginner’s Path

- Part 5: Common Pitfalls and Avoidance Guide

- Summary

- FAQ (Frequently Asked Questions)

You May Have Already Encountered On-Chain Assets

I initially thought the term “on-chain assets” sounded quite intimidating.

But if you’ve ever bought a fund through Alipay or paid a bill via WeChat Pay, you’ve already encountered the concept of “asset digitization.” On-chain assets go a step further—they don’t require banks or brokers; you truly own them, rather than having them “custodied by a third party.”

Frankly, in 2026, on-chain assets are no longer just toys for geeks. From Bitcoin and Ethereum to tokenized U.S. Treasury bonds and fractionalized real estate, “going on-chain” is changing our definition of “ownership.”

You may have seen these in the news:

- Bitcoin ETF approved, Wall Street giants rushing in

- Hong Kong and Singapore launching digital asset exchange licenses

- A real estate company selling a building as 10,000 fractions on-chain

- Central Bank Digital Currencies (CBDCs) being piloted in multiple countries

Behind all these is the logic of on-chain assets.

In this article, I’ll use the most down-to-earth approach to help you understand the underlying logic of on-chain assets. Whether you’re a complete beginner or have heard about it but not fully grasped it, after reading this, you’ll understand:

- What on-chain assets really are

- How to choose and use a wallet

- Why RWA is so hot

- How beginners can start safely

Part 1: What Exactly Are On-Chain Assets?

In Simple Terms: “Value Certificates Stored on the Blockchain”

Traditional assets, like the money in your bank account, are essentially a string of numbers in a bank’s database. The bank says you have 1 million, so you do; if the bank’s system fails, your 1 million might temporarily “disappear.”

On-chain assets are different. They exist on the blockchain—think of it as a massive ledger maintained by thousands of computers worldwide. Your assets are recorded on these computers, not on a single company’s server.

Three core features:

- Truly yours — As long as you keep your private key safe (more on this later), no one can freeze, confiscate, or tamper with your assets.

- Global circulation — No need for currency exchange or bank business hours; send to anyone on Earth anytime.

- Transparent — Every transaction is traceable, but your identity is anonymous (using an address instead of a name).

What Is Blockchain? Simply Put: “Everyone Keeps the Books Together”

You may have heard blockchain is complex, but the core logic is simple:

Imagine a class ledger. Previously, one class monitor (the bank) kept everyone’s accounts. Now, every student has their own ledger, and every time someone transfers money, everyone records it. If someone tries to alter their record, they need approval from more than half the class—which is nearly impossible.

That’s the essence of blockchain: distributed ledger + consensus mechanism.

Common Types of On-Chain Assets

| Type | Example | Plain Explanation | Risk Level |

|---|---|---|---|

| Native Tokens | BTC, ETH | The blockchain’s “fuel” and “shares” | High volatility |

| Stablecoins | USDT, USDC | ”Digital dollars” pegged to USD, 1 = $1 | Low |

| Governance Tokens | UNI, AAVE | Like stock voting rights, decide project direction | Medium-high |

| NFTs | Digital collectibles, game items | Unique digital ownership proof | Very high |

| RWA Tokens | Treasury tokens, real estate fractions | On-chain versions of real-world assets | Medium |

A Down-to-Earth Example

You buy a concert ticket. Traditionally, Ticketmaster gives you a QR code; if their server goes down, your ticket might be gone. With an NFT ticket, it’s in your wallet, no one can take it, and you can resell it to a friend without platform fees.

Another example:

You’re studying abroad, and your mom wants to send living expenses. Traditional method: go to the bank, fill out forms, exchange currency, pay fees, wait 3-5 business days. On-chain method: Mom operates on her phone, arrives in 5 minutes, fees a few dollars.

That’s the charm of on-chain assets: cut out the middleman, peer-to-peer transactions.

On-Chain Assets vs. Traditional Assets

| Comparison | Traditional Assets | On-Chain Assets |

|---|---|---|

| Ownership | Custodied by bank/broker | Self-controlled via private key |

| Trading Hours | Business days, working hours | 7x24 hours |

| Cross-border Transfer | 3-5 days, high fees | Minutes, low fees |

| Transparency | Opaque | Fully public and traceable |

| Barrier | Requires bank account | Only needs internet connection |

| Risk | Bank failure risk | Private key loss risk |

Part 2: Wallets—Your Digital Asset Safe

A Wallet Doesn’t Hold “Coins,” It Holds “Keys”

This is a huge misconception.

Your Bitcoin and Ethereum aren’t “stored in a wallet.” They’re always on the blockchain; a wallet is just a tool to manage your private key.

What is a private key?

In simple terms, it’s a very long password. Whoever has this password owns the corresponding assets. So the core function of a wallet is: securely store your private key.

Seed Phrase: Your Only Lifeline

When creating a wallet, the system gives you 12 or 24 English words. This phrase = your private key.

Important enough to say three times:

- Screenshot saving is not allowed!

- Photo saving is not allowed!

- Cloud storage is not allowed!

Correct practice: Write it down on paper and keep it in a fireproof, waterproof place. Some people store it in a bank safe deposit box, others use metal seed phrase plates. I’ve seen too many people lose tens of thousands of dollars in assets forever because they lost their seed phrase.

Things you must never do:

- Save the seed phrase in WeChat favorites

- Screenshot and save to your photo album

- Send it to anyone (including “customer service”)

- Store it in email or cloud storage

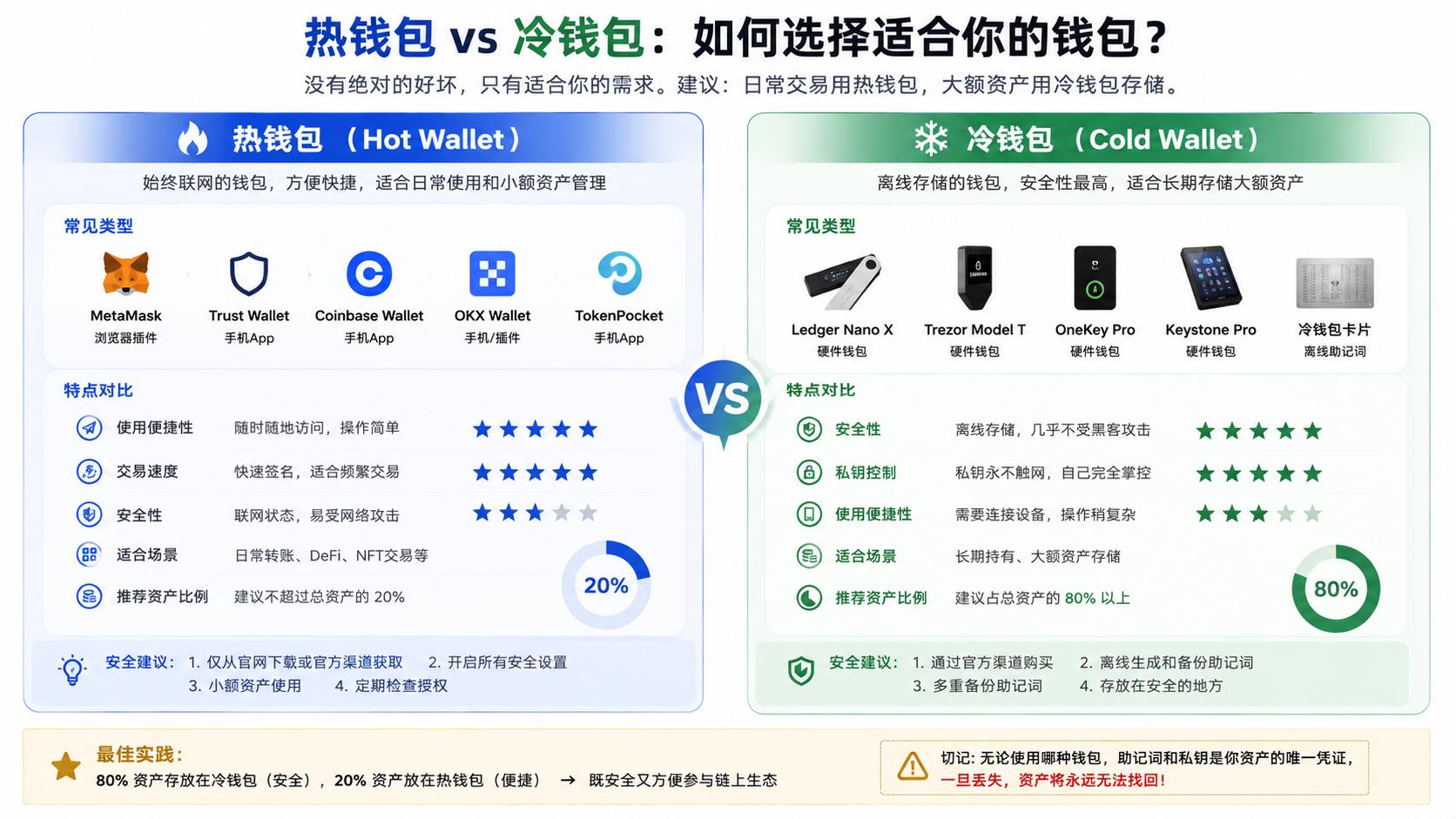

Hot Wallets vs. Cold Wallets

I once struggled with this too, but it’s actually simple:

Hot Wallets (mobile apps, browser extensions)

- Pros: Convenient, trade anytime

- Cons: Connected to the internet, risk of being hacked

- Suitable for: Small daily use, frequent trading

- Recommended: MetaMask, Trust Wallet, Rainbow

Cold Wallets (hardware devices, paper seed phrases)

- Pros: Not connected to the internet, extremely secure

- Cons: Slightly more cumbersome to operate

- Suitable for: Large storage, long-term holding

- Recommended: Ledger, Trezor, OneKey

My advice:

- Most assets (80%) → Cold wallet (e.g., Ledger, Trezor)

- Daily trading funds (20%) → Hot wallet (e.g., MetaMask, Trust Wallet)

It’s like not carrying all your wealth in your pocket while shopping; most is in the bank, only daily cash on hand.

How to Create Your First Wallet

Using MetaMask as an example:

- Download: Always download MetaMask wallet only from the official website. The only official URL is metamask.io. Do not download through any third-party links to avoid asset theft.

- Create: Select “Create a new wallet”

- Backup: The system displays 12 seed words; write them down by hand

- Verify: Click the words in order to prove you’ve backed them up

- Set Password: This password is just the app lock; the seed phrase is the foundation of your assets

Common beginner mistakes:

- Confusing the password with the seed phrase

- Depositing funds without backing up the seed phrase

- Operating the wallet on public WiFi

What Is a Wallet Address?

Each wallet has an address, like: 0x1234…5678

You can think of the address as a “bank account number.” For someone to send you money, they only need this address.

Important reminders:

- Different blockchains have different address formats (Bitcoin, Ethereum, Solana are all different)

- Always confirm the address and network match when transferring

- Sending to the wrong chain or wrong address may result in permanent loss of coins

Part 3: RWA—Real World Assets on the Blockchain

RWA Is the Hottest Concept in 2026, Bar None

RWA stands for Real World Assets, which translates to “real-world assets on the blockchain.”

What does it mean?

It means turning traditional assets like houses, stocks, gold, and government bonds into tokens on the blockchain. An asset can be split into thousands or tens of thousands of fractions, and people worldwide can buy, sell, and trade them.

Why Do This?

Honestly, it’s quite appealing:

For asset owners:

- Expanded financing channels, no longer limited to local investors

- 24/7 trading, significantly improved liquidity

- Settlement from T+2 to minutes

- Reduced intermediary costs (fewer lawyers, accountants, custodians needed)

For investors:

- Buy fractions of U.S. Treasury bonds for as little as $100, extremely low barrier

- Global asset allocation becomes simple

- Real-time income, no waiting

- High transparency, can track asset status anytime

Real-World RWA Examples

| Asset Type | Representative Project | How It Works | Expected Return |

|---|---|---|---|

| U.S. Treasury Bonds | Ondo Finance | Buying tokens equals buying U.S. Treasuries, 4-5% annual yield | 4-5% APY |

| Real Estate | RealT, Lofty | Buy real estate fractions, receive rental dividends | 8-12% APY |

| Private Equity | Centrifuge | SME accounts receivable financing | 10-15% APY |

| Commodities | Paxos Gold | 1 token = 1 gram of physical gold | Follows gold price |

| Private Credit | Maple Finance | Institutional lending market | 8-12% APY |

I tried Ondo’s dollar yield token last year; the experience was amazing:

- Traditional way to buy U.S. Treasuries: Open an account, identity verification, minimum $100,000 investment, T+2 settlement

- RWA way to buy U.S. Treasuries: Connect wallet, done in minutes, $100 minimum, real-time settlement

Income is sent directly to your wallet, settled daily. This is unimaginable in traditional finance.

RWA Risks to Be Aware Of

Of course, RWA isn’t perfect:

- Regulatory uncertainty — Countries are still figuring out their stance on RWA

- Counterparty risk — Need to verify if the asset is truly backed

- Smart contract risk — Code vulnerabilities could lead to losses

- Liquidity risk — Some RWA tokens have low trading volume, potentially high slippage when selling

- Compliance costs — Quality RWA projects require significant compliance investment

So my advice: Start with small amounts, choose projects with clear backgrounds and compliant qualifications.

RWA Development Trends in 2026

- More countries introducing RWA-friendly policies

- Traditional financial institutions entering in force

- Accelerated tokenization of real estate and private equity

- Regulatory frameworks gradually becoming clearer

Part 4: How to Play with On-Chain Assets? Beginner’s Path

Step 1: Create a Wallet

Recommended: Use MetaMask (Little Fox Wallet), available as browser extension + mobile app.

Process: Download → Create wallet → Write down seed phrase (by hand!) → Set password → Done

Step 2: Understand Gas Fees

Every transfer or transaction requires a Gas fee, think of it as a “blockchain usage fee.”

- Ethereum mainnet Gas fees are higher, tens of dollars during peak times

- Layer2 (like Base, Arbitrum) is much cheaper, a few cents

- Gas fees vary by time; trading during off-peak hours is more cost-effective

Tip: Use Ultrasound.money to check real-time Gas fees and operate during low periods.

Step 3: Buy Coins from an Exchange and Withdraw to Wallet

- Register and complete identity verification on exchanges like Binance, OKX

- Buy USDT (stablecoin) with fiat currency

- Withdraw coins from the exchange to your wallet address

First-time operation advice:

- Transfer a small amount first (e.g., $10) to test

- Confirm receipt before transferring larger amounts

- Double-check the address; sending to the wrong chain or address means permanent loss of coins

Step 4: Explore the On-Chain World

Once you have coins in your wallet, you can:

DeFi Lending

- Deposit USDC into Aave, Compound to earn interest (currently 3-8% APY)

- Participate in liquidity mining (higher returns but higher risk)

- Note: Choose established projects, avoid high-yield traps

Buy RWA

- Buy U.S. Treasury tokens through Ondo

- Buy real estate fractions through RealT

- Buy gold tokens through Paxos

Trade Other Tokens

- Trade on decentralized exchanges like Uniswap

- Note: Many small coins are scams; only buy what you understand

Collect NFTs

- Buy digital collectibles on OpenSea

- Note: NFT market is highly volatile; invest cautiously

Step 5: Learn to Use Blockchain Explorers

Recommended tools:

- Etherscan: Ethereum blockchain explorer, can check all transaction records

- DeBank: Multi-chain asset tracking tool, view all assets in one place

- Zapper: DeFi portfolio management

A Mistake I Made

Initially, for convenience, I kept most of my assets on an exchange. Then I saw news about an exchange being hacked, causing user asset losses. Although some were compensated, the feeling of “assets not under my control” was terrible. Now, 95% of my assets are in a cold wallet, with only 5% on exchanges for trading convenience.

Part 5: Common Pitfalls and Avoidance Guide

Pitfall 1: Phishing Websites

Fake websites that look identical to real ones, tricking you into entering your seed phrase.

How to avoid:

- Only download apps from official websites

- Bookmark frequently used sites; don’t click links in emails

- Check the URL (MetaMask’s official site is metamask.io, not metamask.com)

Pitfall 2: Fake Customer Service

“Hello, I’m customer service from XX exchange. Your account is abnormal; please provide your seed phrase for verification.”

Truth: No legitimate platform will ever ask for your seed phrase.

Pitfall 3: Scam and Pyramid Tokens

“Invest $1,000, get your money back in a month, triple in three months.”

Truth: 99% are scams. Only buy projects you understand; avoid high-return promises.

Pitfall 4: Malicious Contract Approvals

Some DApps ask you to approve “unlimited allowance” and then drain all your assets.

How to avoid:

- Use revoke.cash to regularly check approvals

- Revoke unused approvals promptly

- Only approve necessary amounts

Pitfall 5: Private Key/Seed Phrase Leak

- Screenshot saved → Photo album synced to cloud → Hacked

- Copied to clipboard → Phone infected → Read

Correct practice: Write by hand, store physically.

Summary

On-chain assets aren’t some mysterious high-tech; they simply give us a new way of “ownership.”

Remember three core points:

- Private key = Assets — Keep your seed phrase safe, and you keep your assets safe

- On-chain = Autonomy — No permission needed; your assets truly belong to you

- RWA = Bridge — Traditional finance and the crypto world are merging; opportunities are abundant but caution is needed

In 2026, on-chain assets have moved from the fringe to the mainstream. Bitcoin ETF approval, Wall Street giants entering, central banks researching digital currencies—the trend is clear.

Of course, risks always exist. My advice: Use money you can afford to lose, keep learning, and explore slowly.

FAQ (Frequently Asked Questions)

Q1: What is the difference between on-chain assets and money in a bank account?

A: The core difference is ownership and control.

Money in a bank account is a debt the bank owes you; the bank can freeze or restrict your usage. In 2022, there was news about a bank system upgrade leaving users unable to withdraw money for days. On-chain assets are truly yours; as long as you keep your private key safe, no one can freeze, confiscate, or tamper with your assets.

But the trade-off is: You are responsible for security. If you lose your seed phrase, no “customer service” can help you recover it. Banks have deposit insurance; on-chain assets do not.

Simple analogy:

- Bank account = Locker, key held by the bank

- On-chain assets = Home safe, key held by you

Q2: How much money does a beginner need to start? How to begin?

A: $100 is enough to start. Follow these steps:

Learning Phase ($0)

- Download MetaMask, create a wallet

- Learn basic operations, don’t deposit money

- Watch tutorials, join communities to ask questions

Trial Phase ($50-100)

- Buy a small amount of USDT on an exchange

- Practice withdrawing coins to your wallet

- Try simple transfer operations

Practice Phase ($500-1000)

- Try DeFi lending (e.g., deposit on Aave)

- Buy a small amount of major coins (BTC, ETH)

- Experience RWA products (e.g., Ondo U.S. Treasuries)

Important reminders:

- Don’t go all in, and never borrow to invest

- Only play with money you can afford to lose

- Learn to walk before you run

Q3: Are on-chain assets safe? Can they be stolen?

A: The blockchain itself is secure, but your operations may not be.

Why blockchain is secure:

- Decentralization: No single point of failure

- Encryption: Private keys cannot be cracked

- Transparency: All transactions traceable, high cost of malicious acts

Why coins still get lost:

- Seed phrase leak (most common)

- Clicking phishing links

- Approving malicious contracts

- Exchange hacks (not your fault, but assets are affected)

Security advice:

- Use cold wallets for large amounts, hot wallets for small amounts

- Write down seed phrases by hand, store physically

- Don’t click unknown links, don’t scan unknown QR codes

- Regularly check approvals, revoke unused ones

- Don’t use DApps from unknown sources

Q4: What is the difference between RWA and buying traditional financial products?

A: The core differences are efficiency, barrier, and transparency.

| Dimension | Traditional Finance | RWA |

|---|---|---|

| Trading Hours | Business days, fixed hours | 7x24 hours |

| Settlement Time | T+1 or T+2 | Minutes |

| Minimum Investment | Usually $10,000-$100,000 | A few dollars |

| Transparency | Not public | Traceable on-chain |

| Intermediary Costs | High (multiple layers) | Low (smart contract automation) |

| Regulatory Maturity | Mature | Still developing |

Specific example: Buying U.S. Treasury bonds

- Traditional: Open account, identity verification, minimum $100,000, T+2 settlement

- RWA: Connect wallet, done in minutes, $100 minimum, real-time settlement

However, RWA’s regulatory framework is still evolving, and compliance is less mature than traditional products. Choose projects with compliant qualifications.

Q5: Where can I learn more? What learning resources are available?

A: Recommended resources, from beginner to advanced:

Chinese resources:

- Mirror.xyz — Many high-quality Web3 educational articles; search for “on-chain assets,” “DeFi beginner”

- Chain Catcher — Industry news and in-depth analysis

- Odaily — Blockchain news media

English resources:

- Bankless Newsletter — Weekly industry updates, good for tracking trends

- CoinGecko Learn — Systematic beginner tutorials

- Ethereum.org — Official Ethereum learning resources

Tools:

- DeBank: Track multi-chain assets

- Zapper: Manage DeFi portfolios

- CoinGecko: Check prices, market cap, project info

Communities:

- Join one or two quality Discord communities (e.g., official Bankless, HashKey groups)

- Get timely answers to questions

- But don’t trust “investment advice” from strangers in the group

Q6: What is Gas fee? How to save money?

A: Gas fee is a “blockchain usage fee” paid for every transfer or transaction.

Why Gas fees exist: The blockchain network is maintained by global miners/validators; Gas fees are their reward.

Money-saving tips:

- Operate during off-peak times (weekends, U.S. early morning)

- Use Layer2 networks (like Base, Arbitrum), Gas fees are 90%+ cheaper

- Batch operations, avoid frequent small transfers

- Use ultrasound.money to check real-time Gas fees

Gas fee comparison across networks:

- Ethereum mainnet: Peak $20-50, off-peak $5-10

- Layer2 (Base/Arbitrum): Usually $0.1-1

- Solana: Usually below $0.001

Q7: Do I need to pay taxes on on-chain assets?

A: In most countries/regions, gains from on-chain assets need to be declared for tax purposes.

General rules:

- Profit from buying/selling crypto = capital gains, needs to be reported

- Mining, staking rewards = ordinary income, needs to be reported

- Policies vary by country; consult a local tax professional

Record-keeping advice:

- Keep all transaction records

- Use tools like Koinly, CoinTracker for automatic calculation

- Even if exchanges don’t proactively report, it’s advisable to comply voluntarily

Q8: Why is my transaction “stuck”?

A: Usually due to setting the Gas fee too low.

When the blockchain network is congested, miners prioritize transactions with higher Gas fees. If your Gas fee is too low, the transaction may remain pending.

Solutions:

- Wait: It will be processed automatically when the network is less congested

- Speed up: Resend with a higher Gas fee

- Cancel: Send a “null transaction” with a higher Gas fee to override

Q9: Can I share my wallet address with others?

A: The address can be public, but the seed phrase/private key absolutely cannot.

- Address = Bank account number: Share it so others can send you money

- Seed phrase = Bank card password: If leaked, your assets are lost

Privacy advice:

- Use different addresses for different purposes

- Don’t use publicly exposed addresses for large assets

- Can use mixing tools like Tornado Cash (be aware of compliance risks)

Q10: Is it too late to enter now?

A: There’s no standard answer, but here are some perspectives.

Optimists believe:

- Bitcoin ETF approved, institutional money entering

- Central banks researching digital currencies, infrastructure improving

- Web3 applications on the verge of explosion

- Compared to traditional finance, on-chain asset penetration is still low

Cautious people believe:

- High regulatory uncertainty

- Extreme market volatility

- Many projects are just hype

My advice:

- Try with money you can afford to lose

- Don’t FOMO (fear of missing out), don’t FUD (fear, uncertainty, doubt)

- Long-term learning is more important than short-term speculation

- Over a 5-10 year horizon, current fluctuations are just ripples