What is DeFi? A Complete Beginner's Guide to Decentralized Finance | 2026 Update

What is DeFi (Decentralized Finance)? Understand DeFi's core concepts, how it works, mainstream protocols, and hands-on steps for beginners. Latest 2026 data, perfect for absolute beginners with zero knowledge.

Table of Contents

- TL;DR Summary

- Lesson 1: What is DeFi? Explained in Plain English

- Lesson 2: Four Core DeFi Use Cases

- Lesson 3: Three Steps for Beginners

- Lesson 4: DeFi Rewards and Risks

- Lesson 5: Common DeFi Terms Quick Reference

- Summary

- FAQ

TL;DR Summary

DeFi (Decentralized Finance) uses blockchain technology to replace banks, allowing you to directly earn interest on deposits, borrow, and exchange currencies—everything is automated by code, with no human intervention and no middlemen taking a cut. In 2026, DeFi’s total value locked is approximately $80 billion, with Aave, Uniswap, and Lido accounting for half of that.

Lesson 1: What is DeFi? Explained in Plain English

Let’s Start with an Example, Not a Definition

You deposit $10,000 in a bank at an annual interest rate of 0.25%. The bank then lends it out at 4% to someone else. Over a year, you earn $25, and the bank earns $375.

Now imagine a different world: Your $10,000 becomes a line of code, lent directly to someone who needs it. The borrower pays 5% interest, and it all goes to you—because there’s no bank, no tellers, no manager salaries to pay.

That’s DeFi.

Formal Definition

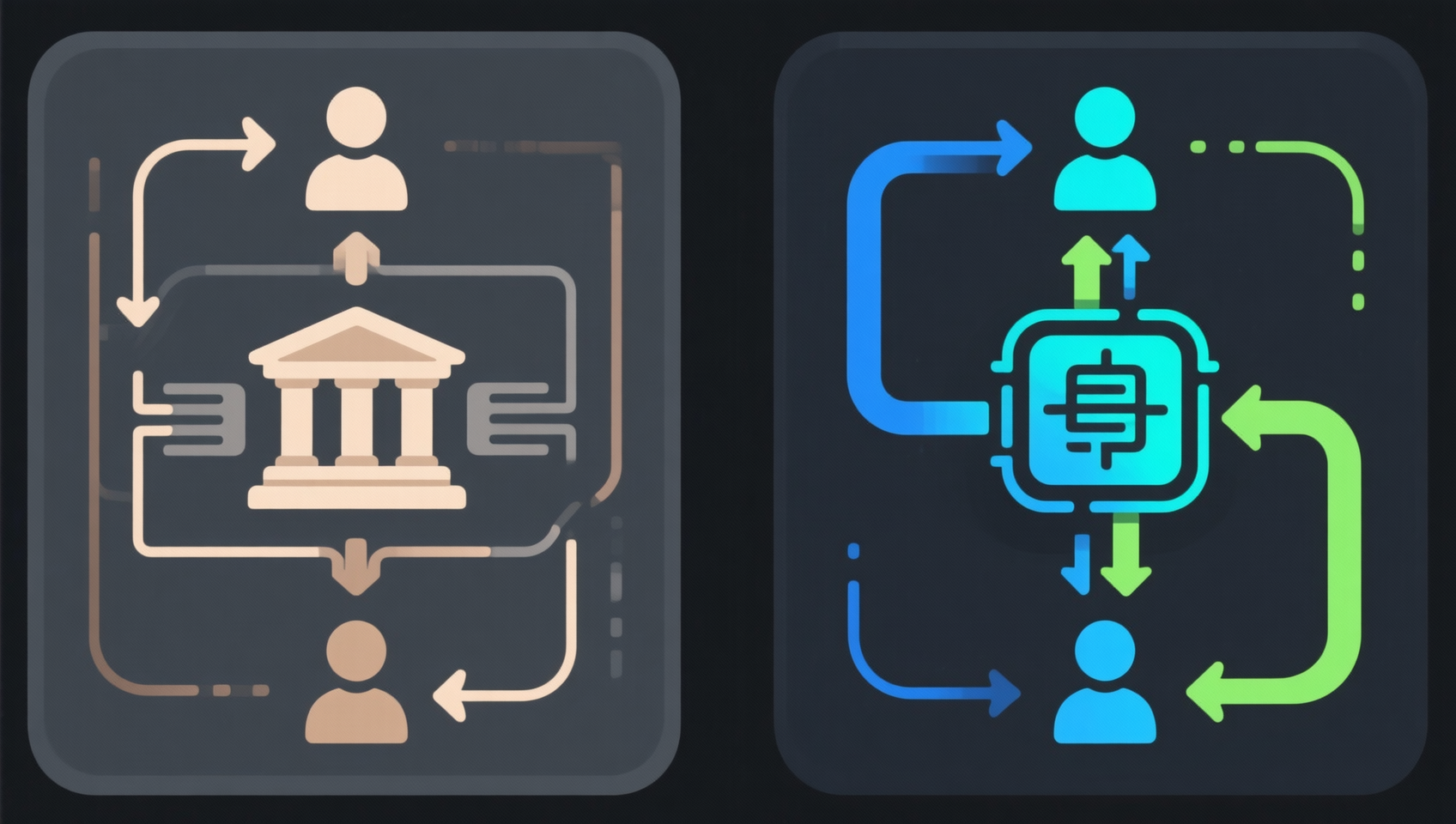

DeFi = Decentralized Finance

It’s not a company or an app, but a set of financial protocols running on a blockchain. Anyone can use it without registering an account or submitting ID—just an internet connection and a crypto wallet.

Core Comparison with Traditional Finance

| Aspect | Traditional Finance (Bank) | DeFi |

|---|---|---|

| Who do you deposit with? | A bank (an institution) | A smart contract (a line of code) |

| Who controls your money? | The bank can freeze/restrict | Only you |

| What do you need to use it? | ID, proof of address, credit history | Just a wallet |

| Operating hours? | Weekdays 9-5 | 24/7/365, never rests |

| Who sets interest rates? | Central bank + bank | Market supply and demand |

| Cross-border transfers? | 3-5 days, high fees | Minutes, cents |

When I first encountered DeFi, I thought: “Isn’t this just a decentralized Alipay?” But after diving deeper, I realized the biggest difference isn’t the technology—it’s ownership. Your money in Alipay is what Alipay owes you; in DeFi, your money is directly controlled by you.

Lesson 2: Four Core DeFi Use Cases

You don’t need to learn every protocol to understand DeFi. There are just four core use cases. Master these, and you’ll understand 90% of DeFi.

1. Lending Protocols (Most Popular)

Representative Protocols: Aave, Compound

This is the largest and most mature sector in DeFi. You can:

- Earn interest on deposits: Deposit USDC, ETH into the protocol for ~2-5% APY

- Borrow with collateral: Deposit ETH as collateral to borrow USDC for trading

In 2026, Aave’s total deposits are around $20 billion, making it one of the largest liquidity pools in DeFi. Its interest rates are automatically adjusted by market supply and demand—more borrowers mean higher rates; more depositors mean lower rates. No need for a bank board meeting to decide on rate cuts.

Why do so many people use it?

- You don’t need to prove your credit to anyone

- No loan application forms

- With ETH, you can borrow USD instantly

2. Decentralized Exchanges (DEX)

Representative Protocol: Uniswap

Unlike centralized exchanges like Binance or OKX, DEXs don’t require you to deposit coins into a platform. Your wallet connects directly to the protocol for one-click swaps. Uniswap is the largest DEX, with a daily trading volume of ~$1.5-2 billion in 2026.

The biggest advantage of DEXs: Custody is in your hands. You don’t entrust assets to an exchange, so there’s no risk of an “exchange exit scam.” The downside is a higher operational threshold, requiring gas fees and on-chain experience.

3. Staking Protocols

Representative Protocol: Lido

Since Ethereum transitioned to Proof of Stake (PoS) in 2022, users can stake ETH to secure the network and earn rewards. But direct staking requires 32 ETH (about $55,000), and staked ETH can’t be withdrawn anytime.

Lido solves this: You stake any amount of ETH and receive an equivalent amount of stETH (a tradable receipt). stETH can be freely used in DeFi—traded, re-staked in other protocols—while automatically accumulating staking rewards daily. In 2026, Lido’s ETH staking APY is about 3.2%.

4. Stablecoin Protocols

Representative Protocol: MakerDAO (now Sky)

This is DeFi’s “central bank.” You deposit ETH as collateral, and the protocol generates DAI (a decentralized stablecoin, 1 DAI ≈ $1).

Unlike other stablecoins (USDT, USDC), DAI isn’t issued by a company but is backed by over-collateralized on-chain assets. Its transparency and censorship resistance are the strongest—no institution can freeze your DAI.

Lesson 3: Three Steps for Beginners

Preparation

To use DeFi, you need three things:

- A crypto wallet—Recommended: MetaMask or OKX Wallet

- A small amount of ETH—For on-chain transaction fees (Gas)

- A Layer2 network—Recommended: Arbitrum or Base for cheap gas fees

💡 Recommended Exchanges: If you don’t have crypto assets yet, you can buy ETH or USDC with fiat on Binance or OKX, then withdraw to your wallet.

Step 1: Connect Your Wallet to a DeFi Protocol

It’s simple:

- Open MetaMask wallet, switch to Arbitrum network

- Visit Aave’s website (app.aave.com)

- Click “Connect Wallet”

- Confirm the signature

The whole process is similar to “logging into a website with WeChat”—except WeChat uses a username and password, while DeFi uses a wallet signature.

Step 2: Make a Small Deposit

Using Aave as an example:

- After connecting your wallet, you’ll see the deposit page

- Choose the asset you want to deposit (e.g., USDC)

- Enter the amount (recommend starting with $20-$50)

- Confirm the transaction

- Wait a few minutes for on-chain confirmation, then you’ll see your interest growing in real-time

Step 3: Try Borrowing (Optional)

If you deposited USDC into Aave, you can borrow up to about 70% of your deposit—e.g., deposit $100 USDC, borrow ~$70 of another asset.

Remember: If your borrowing ratio exceeds the safety threshold, your collateral will be liquidated (force-sold by the system). Beginners should only deposit, not borrow, to first experience earning interest.

The first time I deposited 50 USDC on Aave, I earned about $0.005 per day. It was tiny, but watching interest automatically credited felt magical—no bank, no approval, code automatically pays you interest. This “disintermediation” feeling is more powerful than reading a hundred tutorials.

Lesson 4: DeFi Rewards and Risks

Where Do Rewards Come From?

| Method | Estimated APY | Risk Level | Suitable For |

|---|---|---|---|

| Stablecoin deposits (Aave/Compound) | 3-5% | ⭐ Low | Everyone |

| ETH staking (Lido) | ~3.2% | ⭐ Low | ETH holders |

| DEX market making (stablecoin pairs) | 5-15% | ⭐⭐ Medium | Advanced users |

| Liquidity mining | 10-100%+ | ⭐⭐⭐⭐ High | Experienced users |

Stablecoin deposits are the best DeFi entry point for beginners—low risk, transparent returns, and instant withdrawals.

Risks You Must Know

-

Smart Contract Risk (Most Severe): A bug in the code could mean your money goes to zero. Solution: Only use top protocols (Aave, Uniswap, Lido, MakerDAO), which have undergone hundreds of audits and have billions in TVL, making bugs far less likely than in smaller protocols.

-

Liquidation Risk (Only When Borrowing): If you borrow USDC against ETH and ETH’s price crashes, liquidation can be triggered. Solution: Beginners should only deposit, not borrow, to avoid liquidation risk entirely.

-

Gas Fee Risk: On Ethereum mainnet, gas fees can reach $50-100 during peak times. Solution: Operate on Layer2 networks (Arbitrum, Base, Optimism), where gas fees are just cents.

-

Operational Risk: Sending to the wrong address, approving malicious contracts, clicking phishing links. Solution: Double-check addresses before every operation, don’t click links from strangers, use Rabby wallet’s security checks.

⚠️ Core Principle: In DeFi, you are your own bank and your own security guard. All rewards are yours, but all risks are yours too. Don’t exceed $100 for your first deposit; spend at least three months getting familiar before considering larger investments.

Lesson 5: Common DeFi Terms Quick Reference

| Term | Chinese | Simple Explanation |

|---|---|---|

| TVL | Total Value Locked | Total value (in USD) locked in a protocol; higher means more popular |

| APY/APR | Annual Percentage Yield/Rate | APY includes compounding; APR is simple interest |

| LP | Liquidity Provider | Someone who deposits funds into a DEX for market making |

| IL | Impermanent Loss | Loss incurred by LPs due to price volatility |

| Liquidation | Liquidation | Forced sale of collateral when its value drops below a threshold |

| Slippage | Slippage | Difference between the order price and execution price |

| Gas | Gas Fee | Transaction fee on a blockchain |

| Collateral | Collateral | Asset pledged when borrowing |

| LTV | Loan-to-Value Ratio | Ratio of borrowed amount to collateral value (higher = more risk) |

Summary

DeFi is not an app or a company; it’s a decentralized experiment in financial infrastructure—allowing everyone to directly participate in financial markets using their own assets, without any intermediaries.

Three Most Important Things for Beginners:

✅ Deposit first, borrow later—Only deposit for interest initially; don’t borrow

✅ Start small—$20-$50 per transaction; increase after getting comfortable

✅ Choose top protocols—Aave, Uniswap, Lido, MakerDAO; safety first

Next Steps:

- On-Chain Wealth Management: How to Earn Interest on Aave and Compound (Coming Soon)

- Crypto Wallet Guide: Cold vs Hot Wallets (Coming Soon)

- What Are On-Chain Assets? From Wallets to RWA Explained

- On-Chain Guide—More blockchain education and on-chain tutorials

FAQ

Q: Do I need to know programming to use DeFi?

Absolutely not. All DeFi protocols have graphical interfaces, similar to banking apps—select a product → enter an amount → confirm. The only extra skill is basic MetaMask wallet usage (creating a wallet, transferring, connecting to protocols), which you’ll learn in one go.

Q: Is it too late to get into DeFi now?

DeFi is still in its early stages. In 2026, DeFi’s TVL is about $80 billion, while the global banking system holds over $150 trillion. DeFi’s penetration is less than 0.1%. Compared to the internet’s growth rate in the 1990s, DeFi has enormous room for growth.

Q: Do I need to pay taxes on DeFi?

In most countries, DeFi earnings are taxable. Interest income from deposits is typically taxed as interest income, and token swaps trigger capital gains tax. Rates vary by country; consult a professional tax advisor and keep transaction records. In China, personal holding and trading of crypto is currently not explicitly taxed, but monitor policy changes.

Q: What is TVL and how do I check it?

TVL (Total Value Locked) is a key metric for measuring DeFi protocol size. Check rankings on DeFiLlama. Higher-ranked protocols are generally safer—Aave ($20B), Lido ($30B), Uniswap (~$5B).

Q: How do I protect my DeFi assets?

Four core habits: ① Only use hardware wallets (Ledger/OneKey) to sign transactions; private keys never touch the internet ② Check approval limits each time and revoke after use ③ Don’t click unknown links; only use bookmarks to access protocol websites ④ Separate management—keep most funds in a hardware wallet untouched; use a hot wallet for operations with small amounts.

Q: There are so many L2 chains; which one should a beginner choose?

Recommend Base or Arbitrum. Base is Coinbase’s L2 with the best user experience, fastest ecosystem growth, and low gas fees. Arbitrum is the largest L2 with the most mature ecosystem, hosting major protocols like Aave and Uniswap. Start with Base, then try Arbitrum.

📚 Further Reading:

- 2026 Beginner’s Guide: What Are On-Chain Assets?

- Top 5 RWA Projects to Watch in 2026

- On-Chain Guide—More blockchain education and on-chain tutorials

Disclaimer: This content is for educational purposes only and does not constitute investment advice. Cryptocurrency investment carries risk; make decisions based on your own circumstances.